The Real Cost of Alternative Financial Services

Buyer beware: Credit is a valuable too but in some cases very costly.

Roughly 20% of the US population, checking account or not, use alternative financial services (AFS). According to the FDIC, nearly half of those are unbanked.

Financial institutions and local banks offer loans and revolving lines of credit that are cheaper than these alternatives below:

Prepaid checking accounts

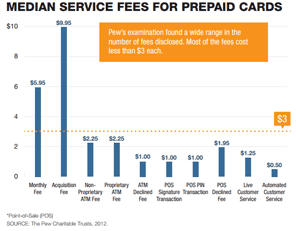

Nearly 10% of all U.S. households do not have a bank account. Since many household transactions cannot be paid in CASH, consumers have to seek reloadable prepaid debit cards. Studies show these cards are risky, largely unregulated and come with varying fee structures and disclosures making it nearly impossible to comparison shop.

The PEW report in 2011, Loaded With Uncertainty: Are Prepaid Cards a Smart Alternative to Checking Accounts? compared over fifty prepaid cards and found:

- Most of the products have dozens of individual fees to consider which sometimes could be cheaper than banks but many times not.

- These cards are not covered by laws regarding full disclosure of fees and terms nor limit consumer liability for unauthorized transactions

- $250,000 FDIC deposit insurance does not always apply and there is no guarantee you are protected since many prepaid cards are not required to carry insurance at all

Payday loans

These are high-cost, short-term loans with the principal due in full plus interest and fees on the borrower's next pay date.

You should only use in an emergency situation. Before you sign for one of these loans, please make sure you fully understand the lender's terms and conditions, APR and fees, repayment schedule and rollover and extension policies.

If you think you won't be able to pay by the next time you get paid, consider a longer term loan from the same lender (if available) or another financial institution. If you do get a loan and can't pay, contact your lender ASAP and to negotiate a longer term. This may increase the cost of the loan but the implications of non-payment or paying late are far worse.

Check cashing services

Check cashing stores have cashed billions of checks offering consumers quick and convenient ways to cash checks written to them. Many charge a flat 1-3% depending on the amount but competition has brought the discounters in. Walmart charges a $3 fee for checks up to $1000 and $6 for up to $5000.

Ask yourself. Isn't it silly to have to pay to cash a check? Especially when there are plenty of "no fee checking accounts", you just have to look for them. Veterans, seniors, government employees and students are eligible for more; all you have to do is ask.

Rent to own services

These services allow consumers to rent tangible property, such as electronics and furniture, by making monthly or weekly payments with the option to buy at any time during the rental term. The store retains possession until the item is paid for in full and if you miss a payment, the store repossesses it. If you only need the furniture for a short time, it's a win-win and you should definitely take advantage.

Because you are renting a new item, the retail value falls considerably and is practically worthless to the store if you fail to honor your agreement. Rent to own agreements are technically loans but there is never any interest. That doesn't make them cheap since stores will sometimes double the retail value of some of the items while you make payments. These services are a lot more expensive than getting a loan elsewhere to buy the item outright.

Refund anticipation loans

Refund anticipation loans (RAL) were short term loans secured by your income tax return and could be available in as little as 24 hours. Because of their abuse, they are now discontinued and called refund anticipation checks (RAC).

RACs are temporary accounts which wait for your tax refund from the IRS. These are still considered loans and come with similar fees and risks of third-party "cross-collection".

To avoid paying excessive fees and interest with these refund tax loans, manage your finances around tax time and when you e-file, request your tax refund through direct deposit so you are first in line to get your money. In most cases, your refund from the IRS will be in your account within 2 weeks.

QUESTIONS TO ASK BEFORE APPLYING FOR CREDIT TO PURCHASE SOMETHING

- Can I get credit?

- Are there any additional or monthly fees?

- What is the annual percentage rate? (APR)

- Can I afford the monthly payments?

- Do I need this right now?

- Can I wait until I have money to pay for it?

- How much more will I pay if I buy using credit?

TIPS FOR MANAGING YOUR CREDIT

Once you get credit, ALWAYS:

- Use a fraction of your total available credit. Lenders will lower your interest rate over time if they label you as being responsible.

- Pay more than the minimum balance due. Paying off your entire bill each month is even better and companies will extend more credit and promotional offers to you.

- Pay on time or early to avoid late fees and to protect your credit record. Contact your creditor immediately if you cannot pay on time. Depending on your situation, they may waive late fees and allow you to make different payment arrangements.

- Check your monthly statements, either online or in the mail. If someone has fraudulent used your credit card and you do not check, you could be on the hook for the charges if you don't catch it in time.

- Compare the difference in cost if you purchase in cash or if you buy with credit

- Check your credit report for free at AnnualCreditReport.com. The federal government setup this site and once a year, consumers can get a free credit report from the three major credit bureau's (Experian, TransUnion, Equifax) NO STRING ATTACHED.